Increasing Dialogue

Many will attest to increasing dialogue around carbon, climate, and regenerative methods in natural resource-based businesses today. This is driving a new query and focus among land buyers and landowners, ranging from the desire to ensure that management practices match the microenvironment to the craving for sequestering carbon and participation in a budding carbon market. Today’s carbon market in the United States is in development. There is a major push across private industry and the public sectors to provide a path forward that incentivizes landowners to both lower emissions and sequester carbon.

The Historical Carbon Market and Today’s Evolving Options

The carbon market garners a great deal of interest from recent and prospective buyers of agricultural land. The carbon market has yet to develop in terms of size, sophistication, and consistency. Historically, participation has focused on traditional emissions-heavy industries such as power generation and energy refiners. These businesses found formal participation through cap-and-trade style arrangements. Individual states offer programs for businesses to curb and/or offset emissions through abatement contracts. This approach is not new and became more formal out of the Kyoto Treaty and the era of acid rain awareness. From 2003 through 2010, the Chicago Climate Exchange operated with 400 members, such as Ford and DuPont, with a reported 680 million tons of carbon traded over the seven-year period. Activity dwindled with the exchange closing by the end of 2010.

Now, there is a realigned climate objective to manage carbon emissions, with two paths emerging with varying degrees of overlap. There is minor momentum in agriculture by a handful of entities to offer programs for farmers and ranchers that focus on reaching zero carbon emissions. Individual operations go through an accounting-style process to credit and debit all emission-intensive practices. The goal is to decrease carbon emissions from daily activities. This is similar to a much more established goal across energy-intensive industries to develop goals for zero emissions during the coming decades.

Rather than directly focusing on net emissions, the second option is increasing carbon sequestration relative to historical storage and selling that additional stored carbon to a willing buyer. Two years ago, Rupert Murdoch’s Australian ranches were nearing completion of the first major carbon sale accomplished by a beef cattle production operation. The third-party entity that structured and monitors this transaction is based in the US. In the last 24 months, they began facilitating transactions in the US, primarily in the state of Texas. According to the University of Texas, there are 65,000 acres under contract in Texas to increase the amount of carbon sequestered on rangeland as of October 2021. The reported prices traded were around $16.50 per ton of carbon sequestered with a contract period of 10 years. The buyers are not directly listed, and access to the market appears to be driven by third-party entities that connect buyer and seller.

Steps of Implementation

Finding who does what in a functioning carbon market is daunting while also being a necessity for those who wish to participate. At this stage, four primary participants are landowners, developers/registries, verifiers, and buyers. There are other secondary participants, including soil scientists, exchanges, attorneys, and project consultants. The steps in transacting a ton of carbon are equally convoluted with a variety of protocols, time horizons, storage measurement methods, and physical opportunities.

The Possible Players

Increasing carbon storage beyond the steady state baseline requires the participation of a landowner. It can be argued that landowners have long been accomplishing this by improving technology and employing best practices on their land as new methods are developed and adopted. To accomplish a tradeable credit, landowners identify a project approach that is recognized in the carbon credit system. Two common projects are taking annual crop production out of a farming rotation to be replanted into a perennial grazing pasture and intensive grazing with decreased pasture size.

Developers are intermediaries who work along with the landowner to ensure these projects are recordable in the marketplace. This includes providing methods and documentation on the amount of carbon storable beyond the baseline. Developers do incentivize the above-referenced projects via direct payments based on carbon values and by providing financing for land use changes. This can range from financing water distribution systems to fencing necessary to change pasture design. It is important to note that developers often take ownership of carbon stored beyond baseline while essentially leasing the storage rights from the landowner. Thus, developers sell the carbon rather than the landowner.

Accessing a registry is key in packaging a carbon project into a tradeable product capable of being transferred to a buyer. The Murdoch Australia project is registered on the Regen network. Regen is responsible for monitoring the amount of carbon sequestered on the ranch. Microsoft bought the future carbon sequestration stream through Regen. Regen employees satellite imagery that measures the change in carbon storage annually. The first year requires direct soil samples using standard methods to calibrate a base satellite image. Other registries, Native, for example, use only direct soil samples on a much longer time horizon.

Soil Types and Carbon Storage

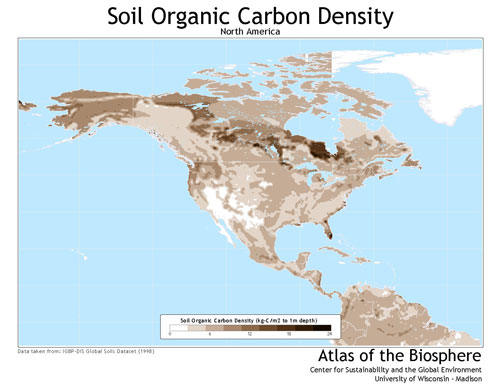

The amount of carbon stored is evaluated by the amount of Soil Organic Carbon (SOC) present in the soil. Below is a map of North America that illustrates SOC levels across regions and land types.

Notice that the 6-9 density region extends in a thin band running north from the Great Salt Lake, then bending west into the 9-12 region along the Canadian border. The darkest shade of that area is the heavily forested areas of western Montana, and the thin band of 6-9 is the timber along the ID-WY border moving north through the headwaters of the Missouri River. Outside of the forest with mixed grasslands, density drops to 3-6kg of carbon per square meter.

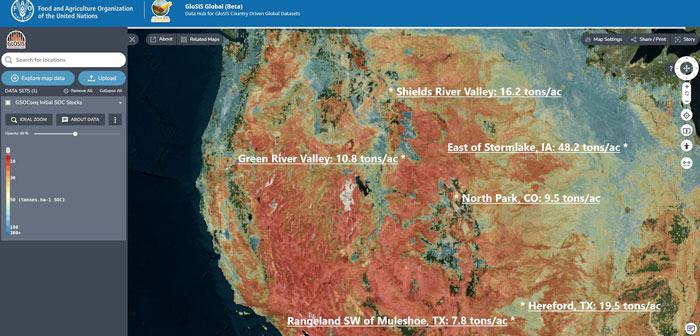

Below is another view framing variables in a metric that is more meaningful to land area and carbon relative to the underlying soil profile. These data are calculated using the UN’s FOA global mapping software. The shading of the map corresponds with the legend on the left that is reported in metric tons per hectare. Conversions to short tons per acre are reported for select areas from Texas to Montana, with locations of interest between.

It appears that the easiest locations to increase soil carbon storage by one ton per acre are those with existing high levels of carbon, given the percentage of change is the least. Growing season, soil type, and precipitation also significantly impact levels of carbon storage potential. These variables coincide with the agricultural carbon sequestering movement gaining a foothold throughout the Midwest, where cover crops and more intensive crop seeding methods can be altered for a greater storage impact. As the process is evolving recently, more inquiries are surfacing along the high plains and foothill regions.

It is critical to note that at least one major registry and facilitator explicitly states they are only interested in land that is denigrated. That implies there is a limitation to rangeland in good to excellent condition where soils, precipitation, and growing season cap natural carbon storage potential. A pattern in registry documents implies that longer-term projects are more suitable in these situations and will be more like a conservation easement. This will serve to offset the shortfall in direct carbon dollarization that others internalize by selling more rapidly accumulating carbon credits.

Another consideration on large-scale land holdings is the acreage breakdown between soil profiles and historical use. For example, the IX Ranch near central Montana is spread over 134,000 acres however, the greatest carbon storage potential is limited to approximately 4,500 acres of ground currently in dryland crop production. The storage potential on this lesser acreage within the ranch is driven by reverting an annual planting rotation into a perennial crop with several varieties that will stimulate greater plant root activity. The remaining balance of acreage, under best rangeland management practices for the given soil profile, will serve more to maintain carbon storage at optimum levels.

The Path Forward

The carbon market is in its early stages and has more than sufficient interest to construct a tradable product. Currently, the limitation is that the market remains fragmented with an opaque group of participants. Buyers are driving for consistency while too many cooks remain in the kitchen. A handful of credible developers and registries will emerge with realistic methods that avoid infringement on private property. Furthermore, many different government agencies are vying for oversight of carbon markets. From the White House to the Commodity Futures Trading Commission and the Department of Transportation, there is a full list of bureaucrats racing to put their stamp on how we manage carbon and emissions. I would like to find a method that allows the landowner to record additional stored carbon as an asset. Currently, carbon stored is transferred to developers who then hold the carbon as an asset that is sold to the buyer. Bottom-line, this is a new space that landowners should watch over the next two years for developments that could offer a sound and sustainable source of cash flow.

Visit more about Carbon with one of our Management Team members.

Author – Jim Fryer, Hall and Hall Management